At a busy truck stop along the Brenner highway, the corridor that connects Italy, Austria, and Germany, dozens of freight trucks lay idle in rows. Drivers refuel their vehicles, check logistics systems, grab a quick meal, and rest before getting back on the road to their destination. These fueling stations are the lifelines of the global freight network – critical infrastructure that keeps trucks, drivers, and goods moving across continents.

This familiar landscape is on the verge of profound transformation. As we stand at the crossroads of an energy transition, fuel retail for freight faces an existential challenge: adapt or risk obsolescence.

The networks of gas stations that we rely on, both as consumers and as logistics professionals, are projected to become unprofitable by 2035 if they maintain their current business models. This isn't just about changing consumer preferences; it's about a fundamental shift in how we power movement across our economy.

In this article, we'll explore how fuel retail is evolving to meet the needs of a changing energy future. We'll examine the emerging technologies disrupting traditional fueling models, the implications for logistics and transportation, and the strategic opportunities for investors. The question is no longer whether fuel retail for freight and consumers will change but how quickly it can transform to remain relevant in our future logistics networks.

Before diving into the specific technologies reshaping fuel retail, it's important to understand why this infrastructure matters to our economy and daily lives.

While XPRESS focuses on the impact on future logistics and freight, we believe that to understand the space fully, we require a comprehensive overview that includes passenger vehicles and aviation.

Fueling infrastructure serves as the backbone of our transportation systems:

The disruption of this infrastructure has far-reaching implications for everything from consumer behavior to supply chain efficiency. As we'll see, each mode of transportation is moving toward its own mix of new fuel solutions, which presents both opportunities for disruption and challenges for infrastructure, investment, and policy.

According to Boston Consulting Group research, fuel retail networks are on track to become unprofitable by 2035, even in scenarios where new mobility models are less disruptive and fossil fuel sales do not decline steeply.

The outlook varies significantly by region:

Fuel retailers that adapt early to the shift toward electrification, alternative fuels, and changing consumer behavior have a chance to build lasting loyalty and brand relevance.

Let’s go through a crash course on the fuels that will power future transportation systems.

Biofuels have gained significant traction since they can be used in existing Internal Combustion Engine (ICE) vehicles after being mixed with traditional fossil fuels. This compatibility with existing infrastructure makes them a critical bridge technology in the energy transition.

Common Types

Cost & Pricing

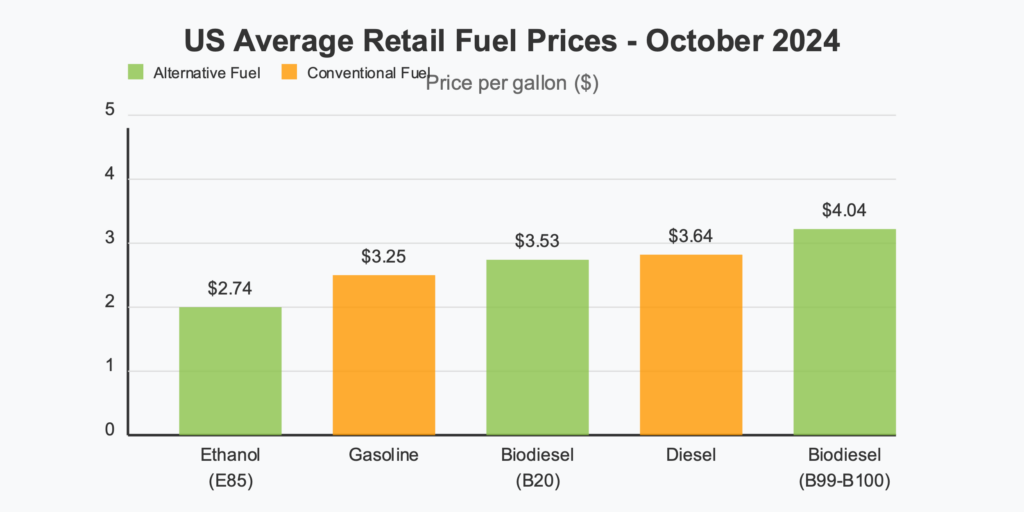

Biofuels pricing varies on feedstock type and source and certification. Additionally, processing and refining require significant infrastructure investments, affecting final prices. Below you can find the average retail prices of Ethanol, Biodiesel (B20), Biodiesel (B99-B100), Gasoline, and Diesel in the US in October 2024, which shows Ethanol as the most affordable option.

Production and Infrastructure

The process of making FAME Biodiesel is called Transesterification Separation and produces Glycerin and pure FAME biodiesel, known as B100.

FAME Biodiesel has limitations due to its higher oxygen content, which can limit storage time due to oxidation, which causes corrosion. Its high freezing point makes it gel-like at low temperatures, preventing flow through fuel lines. For these reasons, FAME is typically blended with diesel for final consumption. Common blends are B5 (up to 5% biodiesel) and B20 (6-20% biodiesel). (FarmdocDaily Illinois University).

Producing both Ethanol and FAME Biodiesel requires more capital-intensive plants. The feedstock is expected to be commoditized and sold instead of the oil itself. Normally, the feedstock is sent to the refineries, and then the oils are mixed in regional distribution centers to produce blends for the end-consumer.

Most Applicable For

Medium-long distances, especially for heavy-duty transport, since electric is too difficult to execute yet due to shorter battery lifecycles and lack of fast charging infrastructure. All vehicle manufacturers allow blends up to B5, and 80% of vehicle manufacturers approve blends of up to B20.

Renewable diesel, aka HVO, is fundamentally different from FAME biodiesel, in that it only contains hydrogen and carbon, making it a hydrocarbon fuel just like petroleum diesel. While not identical to petroleum diesel, renewable diesel is so close that it is considered a “drop-in” replacement for petroleum diesel. In other words, renewable diesel does not need to be blended with petroleum diesel to be used in modern diesel engines. The drop-in nature of renewable diesel is a significant advantage over FAME biodiesel.

Production and Infrastructure

Due to the similar refining process that renewable diesel undergoes, it can be produced in almost the same refineries. Leaders in the petroleum industry are looking to convert existing refineries to produce sustainable fuels such as renewable diesel and sustainable aviation fuel, making the infrastructure faster and cheaper.

Most Applicable For

As with Biofuels, Renewable Diesel (HVO) is best for medium-long distances due to the lack of maturity of other technologies for sustainable heavy-duty transport.

Why Biofuels Matter for Fuel Retail

Biofuels maintain the traditional user behavior of visiting a gas station and taking 5-10 minutes to refuel. This makes them particularly attractive for fuel retailers looking to maintain their business model while transitioning to more sustainable options. As refineries that handle diesel and petroleum partially transition to biofuels, it will be even easier for fueling stations to offer these alternatives since their supply chain remains essentially the same.

Unlike hydrogen or biofuels, electric vehicles (EVs) plug into infrastructure that already exists in nearly every household – which has given them a strategic head start in adoption. While alternative fuels face challenges related to production, transport, storage, and charging hardware, electricity is already universally distributed. This ease of integration has enabled EVs to penetrate the market faster than other sustainable fuel options.

EVs have also benefited from a wave of policy support. The EU announced a ban on new petrol and diesel cars from 2035 in order to reach climate neutrality by 2050 and there have been numerous incentives like tax exemptions, urban-driving benefits, and more in place for a decade already. (European Parliament, German Federal Ministry for Economic Affairs and Climate Action)

Infrastructure

Charging infrastructure is typically divided into three levels:

| Level | Found in | Speed to charge to 80% |

| Level 1 (120V) | Standard home outlets | Very slow: 40-50+ hours to charge a Battery EV (BEV) from 0% to 80% 5-6 hours for a Plug-in-Hybrid EV (PHEV) |

| Level 2 (240V) | Dedicated home or workplace chargers | Average, charging overnight or at the workplace: 4-10 hours to charge a BEV from 0% to 80% and 1-2 hours for a PHEV. |

| Direct Current (DC) Fast Charging (400-900V) | Public high-speed stations | Fastest to date: 20 minutes-1 hour to charge a BEV from 0% to 80% Incompatible with most PHEVs |

Grid Stress and Smart Energy Management

As electric gains market share, the increased load from electric vehicles is becoming a problem for local electricity grids. A single DC fast charger can consume as much electricity as tens of homes during peak usage. (National Renewable Energy Laboratory)

To address this infrastructure challenge, several cities are piloting grid-aware charging strategies:

While Electric Vehicles themselves are more sustainable, the question of how the energy is produced remains. There are initiatives to include solar panels on charge points so that some of the energy is offset with renewable sources, such as those by joint venture of Daimler Truck, the TRATON GROUP, and the Volvo Group, Milence.

Consumer EVs – Maturing Market

Due to their efficiency and expanding charging infrastructure, EVs are considered a great solution for short-haul and urban transport. In 2024 already, they were projected to account for 20% of total car sales. (Virta)

However, this maturing market is still concentrated in specific regions. China, the EU, and the U.S. account for 95% of all EV sales in 2023. (IEA)

Heavy-Duty Trucks – The Frontier

Electric trucks for heavy-duty transport require more developments in battery health and weight, fast charging, and charging infrastructure to reach a state of maturity to take over the market. Heavy batteries reduce payload capacity, directly impacting profitability, while limited range and sparse fast-charging options create range anxiety for decision-maker, dispatcher, and driver alike. Until these issues are addressed, e-trucks are better suited for short-haul and urban routes than long-distance freight.

Urban and regional deliveries, where trips are shorter, and return-to-base patterns allow overnight charging, are already viable use cases of e-trucks. China has dominated this market with over 70% of global electric truck sales in 2023, though this was a decrease from 85% in 2022. In Europe, e-truck sales nearly tripled in 2023, surpassing 10,000 units, representing a market share of over 1.5%. (IEA)

Breakthroughs in Battery Range and Charging Speed

Advances in battery and charging technology are setting new benchmarks faster than expected, pushing electric freight closer to reality.

The Megawatt Charging System (MCS) – capable of delivering up to 3.75 megawatts (MW) of power compared to the existing limit of 350 kilowatt (kW) of standard chargers – is currently being piloted in Europe and the U.S. to support future high-speed charging for freight vehicles. (EVBoosters) Strategic deployment of MCS is planned along major freight corridors, with stations positioned every 100 km to support long-haul trips. This targeted infrastructure will ensure that electric trucks and buses can recharge efficiently during mandatory rest periods, typically around 45 minutes in Europe. MCS presents a huge opportunity for freight’s transition to net zero through electrification.

On the other side of the globe, recent breakthroughs in charging and battery technology could dramatically accelerate the viability of electric freight. In April 2025, Chinese battery giant CATL announced its second-generation Shenxing battery, which adds 520 km of range in just five minutes of charging, surpassing BYD’s previous benchmark (400 km in five minutes) and far exceeding current European or American offerings. With a total range of 800 km and a peak charging power of 1.3 MW, the battery performs even in low temperatures and could support the kind of high-throughput stops needed in freight corridors.

CATL made new additions to its sodium-ion battery line Naxtra, with one type of battery designed specifically for heavy-duty trucks. It offers over eight years of service life and has lower lifecycle costs and higher efficiency than traditional lead-acid batteries. Together, these innovations suggest a future in which electric trucks could realistically recharge during mandatory rest breaks and operate efficiently under demanding freight conditions. (CATL)

Companies such as Milence are working to make electric truck charging infrastructure more commonplace. One group of interested customers are transportation companies that already invested in E-truck fleets, a group that finds itself in an interesting position. It is currently unknown whether the subsidies granted to such companies, like no highway tolls and tax breaks, will continue. If these subsidies end, the benefits of E-trucks might not be enough to outweigh the downsides at the moment.

Investment Opportunities in the EV Fueling Ecosystem for E-Truck Adoption

Whether through public charging networks, the Megawatt Charging System, or home charging, electric has already significantly changed the fueling game. By allowing the customer to fuel in their home, workplace, or parking lot, electric reduces the reliance on traditional fuel retail and forces fuel retailers to keep up.

To support further EV growth, players in the space need to invest in the following areas:

Munich-based startup Fryte is making it easier to bring charging infrastructure directly to where it’s needed – like warehouse parking lots – with a promise of high utilization and predictability. In does this by having a driver-side product which allows drivers and dispatchers to plan charging stops in advance, making the whole system more efficient and less stressful for everyone involved.

Hydrogen Fuel Cell technology is still in its earliest steps compared to the abovementioned types.

Most Applicable For

Hydrogen Fuel is thought to be a good solution for long-haul trucking and heavy transport due to its long range and quick refueling. It takes mere minutes to refuel a Hydrogen cell fuel truck—very similar to diesel but unlike electric, which poses challenges for transportation companies running on operational pressures and low margins.

Hydrogen fuel cell tractors are currently the only viable zero-emission solution proposed for one-for-one replacements for diesel in long-haul heavy-duty trucks.

Production and Infrastructure

The production process for hydrogen fuel cells includes purifying hydrogen to remove contaminants, compressing it to 350-700 bar for storage, and liquefying it to -253°C (for liquid hydrogen storage). Distribution presents a challenge as specialized tanker trucks for compressed or liquid hydrogen and dedicated pipelines are needed. An alternative emerging model is on-site production at fueling stations.

Therefore, widespread adoption of fuel cell technologies depends on lowering the cost of vehicles, building up an international refueling infrastructure, and a sufficient supply of green liquid hydrogen.

Early traction

Daimler has built the first Mercedes-Benz GenH2 truck fleet of five for a customer trial that started in mid-2024. The five semi-trailer tractors will be deployed in long-haul applications on different routes in Germany and refueled at designated public liquid hydrogen filling stations (sLH2) in Wörth am Rhein and the Duisburg area.

While aviation fuel won't be found at traditional fueling stations, Sustainable Aviation Fuels (SAF) deserve mention as they represent another significant shift in the energy landscape.

SAF is produced from biogenic residues such as cooking oils used in the HEFA process (hydro processed esters and fatty acids). When used to 100%, sustainable aviation fuels (SAFs) already certified for use in today’s jet engines produce about 80 percent less greenhouse gas emissions than traditional jet fuel.

Market Challenges

In the retail market, though, SAF currently costs around three times more than traditional jet fuel, which presents numerous challenges.

Regulatory Landscape

The mandates for SAF usage are growing: ReFuelEU Aviation Regulation has set a minimum supply mandate for Sustainable Aviation Fuels (SAF) in Europe, starting with 2% in 2025 and increasing to 70% in 2050. (EASA)

Production

However, in 2024, production capacity was not expected to exceed 1.5 million metric tons (Mt), barely 0.5 percent of total jet fuel needs, according to International Air Transport Association estimates. (McKinsey)

Several aviation industry leaders have expressed the need to build supply of SAF. Scott Kirby, CEO of United Airlines, was quoted saying that the challenge with SAF “is not that supply is limited, the issue is creating supply.” Building a strong outlook for a more sustainable future in aviation includes airlines, governments, and investors investing in SAF production to create the supply needed.

The fuel retail landscape is in the midst of the biggest transformation we’ve seen to date. To remain relevant, fuel retailers will need to embrace several strategic shifts:

Fueling stations will become more modular, containing different fueling options, such as biofuels, electric, and potentially hydrogen in the medium term. This flexibility will allow retailers to adapt to changing market demands and regulations.

First movers offering diesel/gas alternatives will gain a competitive advantage by developing new customer loyalty and brand recognition. As car manufacturers continue to develop engines that allow for higher concentrations of biofuel, stations that offer these options will be well-positioned to capture market share.

If the refineries that handle diesel and petroleum partially transition to biofuels, it will be even easier for fueling stations to offer biofuels since their supply chain stays the same. In addition, the user behavior of biofuels is exactly the same as that of fossil fuels – quick refueling – which unlike electric, offers a seamless transition for biofuels into the fueling station.

While many fueling station companies like Shell are adding and increasing their e-charging capacities, the fact that electric charging can happen anywhere with access to a plug significantly changes the dynamic of fueling retail.

Electric charging democratizes energy access, breaking away from the traditional model of centralized fueling stations. E-fueling your vehicle now becomes a passive behavior – something done at home, at the office, or while shopping, rather than an intentional trip to the gas stop. This deeply challenges the logic of gas stations, especially those where consumers have little to do while they wait.

For that reason, we strongly believe in the emergence of EV charging in locations that have other “main” uses, such as offices, malls, schools, etc. This switch takes the consumer out of the fueling station retail and embeds charging their vehicle organically into their lives.

There is a way to bring the consumer back to the fueling station though. Breakthroughs like CATL’s and BYD’s five-minute, 520 km and 400 km charge introduce a new possibility: if ultrafast charging and extended range batteries become viable at scale, centralized charging hubs could regain their relevance – not because users are forced to go there, but because it’s simply the most efficient option. These megawatt-level systems won’t be feasible in most homes or workplaces due to their enormous power demands. In this scenario, fueling stations have a new opportunity: to reinvent themselves not as gas stops, but as multi-energy refueling centers that offer unmatched charging speed and convenience.

As ultrafast charging becomes possible, fueling stations have a chance to reclaim their role in the EV era. But even with faster chargers, not all vehicles will support 5-minute charging, and many drivers will still spend meaningful time at charging stops.

To survive in this market, fuel retailers need to expand into adjacent value pools like:

No matter the fuel type, stations that offer more than energy will stay relevant in a shifting landscape.

Fuel retailers should consider partnerships with:

These collaborations can help retailers diversify their offerings and remain relevant in a changing market.

As logistics and industrial technology investors, we believe that understanding these dynamics is crucial to identifying the most promising opportunities. While we’re encountering numerous opportunities related to this energy transition, the key questions we're asking include:

Our logistics focus is primarily on road transport, where innovation in fueling stations and infrastructure is critical to supporting the transition to more sustainable options. We believe that the companies that move quickly to position themselves as multi-purpose energy hubs rather than fuel providers will be best equipped to thrive in this new landscape.

If you are building, investing, or thinking about this space – let's connect.

Written by Monika Rodiqi & edited by Newton Davis.